First published on Thomson Reuters Regulatory Intelligence on 20th October 2022.

EMIR Refit leads the global drive for OTC derivatives standardisation

By Emma Kalliomaki, Managing Director, Derivatives Service Bureau (DSB)

On 7 October 2022, the long-awaited revision to the European Markets Infrastructure Regulation (EMIR Refit) was published into the Official Journal of the European Union¹, establishing a formal date of 29 April 2024 for industry implementation and compliance. The publication of EMIR Refit into EU law is the first mandate amongst G20 jurisdictions gearing up to implement enhanced OTC derivatives reporting obligations.

Key amendments to the EMIR technical standards include the introduction of end-to-end reporting in ISO 20022 XML, enhanced and harmonised data quality requirements for data validation and data reconciliation processes across Trade Repositories (TRs), and alignment with international standards to achieve consistency in data elements reported to TRs – such as the Legal Entity Identifier, the Unique Transaction Identifier (UTI), the Unique Product Identifier (UPI) and other critical data elements (CDE).

Development of international standards

The development of international standards for fundamental data elements to report over-the-counter (OTC) derivatives was in response to a request from the G20 Leaders to increase transparency in financial markets, offset systemic risk, and protect against market abuse following the 2007-8 financial crisis.

As a result, the LEI (ISO 17442²), the UPI (ISO 4914³), UTI (ISO 238974) and CDE (included in ISO 20022) standards have been established to improve data alignment and harmonisation across G20 jurisdictions.

The Financial Stability Board (FSB) has been working since the financial crisis to realise the change needed for improved supervision and transparency of OTC derivatives markets. Much of this work has been done in collaboration with industry and has focused on standardisation to improve harmonisation and aggregation requirements.

During this time, immense strides have been made with legal entity/counterparty identification through international implementation and adoption of the LEI. Focus is now on product identification with the development and implementation of the global UPI System, referring to the UPI Code, the UPI Reference Data Library, and the process of assigning a UPI to a set of reference data elements.

The UPI is designed to facilitate the effective aggregation of OTC derivatives transaction reports worldwide, allowing for an improved, consistent view and common understanding of systemic OTC derivative risks. Based on the work of the Committee on Payments and Market Infrastructures and the International Organization of Securities Commissions (CPMI-IOSCO), the UPI Technical Guidance was published in September 2017 and provided the footprint on which the UPI ISO standard was based.

EU leads the way

The EU is the first jurisdiction to formally mandate the UPI, although this is not its first foray into the identification of OTC derivatives. In January 2018, based on MiFIR/MiFID II RTS-23 (reference data reporting) requirements, the scope of the International Securities Identification Number (ISIN – ISO 61665) was extended to cater for the identification of OTC derivatives. Given the continuing international discussions on product identification at that time, the OTC ISIN was developed with the principle of being extendable to multiple jurisdictions and, as far as reasonably possible, consistent with CPMI-IOSCO’s guidance on UPI.

Under MiFIR/MiFID II, the Derivatives Service Bureau (DSB)6 is responsible for serving the needs of OTC derivatives market participants through the allocation and distribution of ISINs, the Classification of Financial Instruments (CFI – ISO 109627) code, and the Financial Instrument Short Name (FISN – ISO 187748). Each standard is complementary to each of the other standards respectively to identify, classify and describe an OTC derivative instrument.

The instrument definitions for OTC ISINs incorporate data elements mandated under MiFIR/MiFID II, which are more granular than required for the generation of UPI. The UPI sits between the CFI and OTC ISIN, with the three components representing an identification framework for OTC derivatives. This model enables market practitioners to understand the relationship between the various standards more easily and aids greater efficiency in assisting with global regulatory reporting obligations.

The DSB as designated by the FSB9 is the sole service provider for the UPI System. Accordingly, the DSB will perform the functions of issuance of UPIs and maintenance of their associated reference data as required by the UPI Technical Guidance and reflected in the ISO UPI standard.

In recent years the European Securities and Markets Authority (ESMA) has focused on harmonisation across reporting regimes. This is seen in EMIR, where OTC ISIN will be the reportable identifier for all instruments with an overlap in scope between MIFIR and EMIR. The UPI will be required for those instruments which are pure OTC derivatives reportable for EMIR only. This will provide consistency for those firms already reporting with OTC ISIN today.

The DSB’s Product Committee, which is comprised of market practitioners and includes authorities as observers, focuses to address issues surrounding data alignment, semantics, interpretation, providing best practice on industry approach, and feeding these issues to authorities. Being under the oversight of the Regulatory Oversight Committee (ROC)10, the DSB is uniquely placed to facilitate continued engagement between private and public sectors to achieve a jurisdiction-agnostic solution.

Staggered adoption

UPI adoption across the G20 is likely to be staggered due to the independent decision-making processes of each jurisdiction. Within each jurisdiction, it is likely that all asset classes will be reportable via a “big bang” approach, with most jurisdictions premised on dual-sided reporting. Reporting timeliness is expected to vary by jurisdiction, with the spectrum ranging from within 15 minutes from execution to T+2.

In relation to specific jurisdiction implementation, the CFTC notice in January 202211 indicated an implementation of Q4 2023 for UPI, based on a 12 month notice period. This will be followed by the EU mandate coming into effect on 29 April 2024. A UK consultation closed in February 2022, with implementation details expected in the coming months.

It is anticipated that the Asia Pacific region will synchronise implementation and work together to ensure harmonisation as far as possible following implementation in the major derivatives markets.

Preparing for implementation

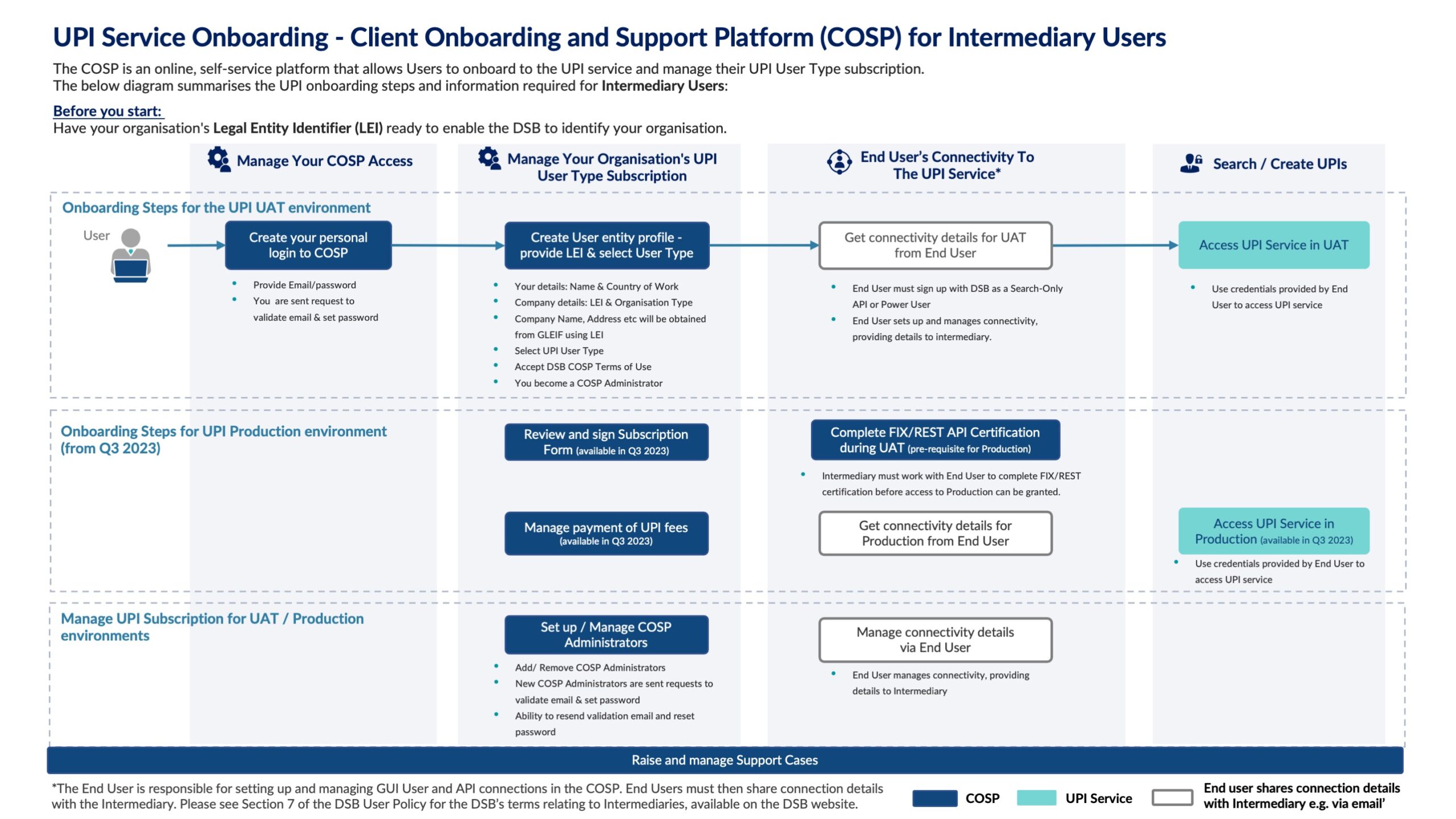

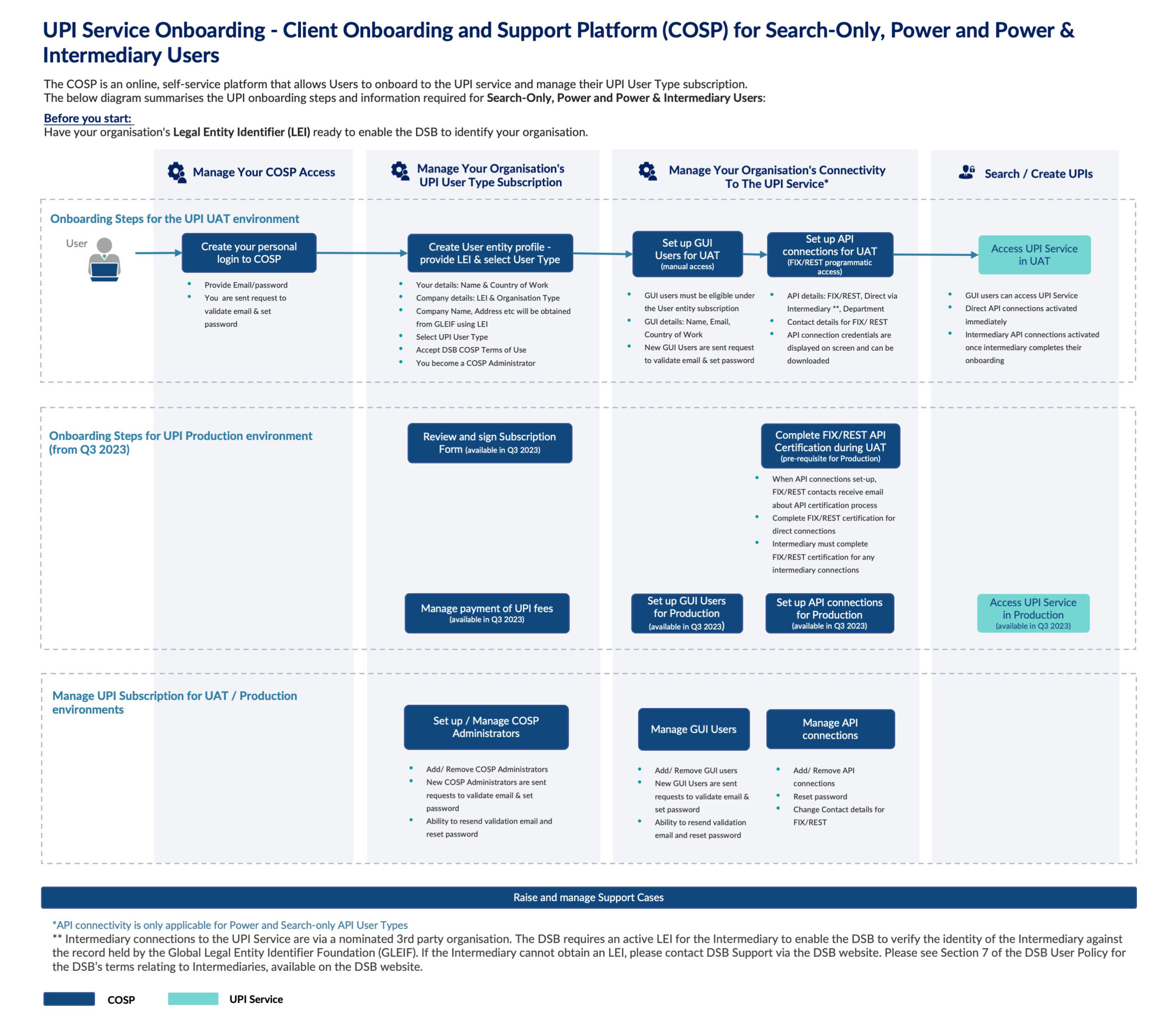

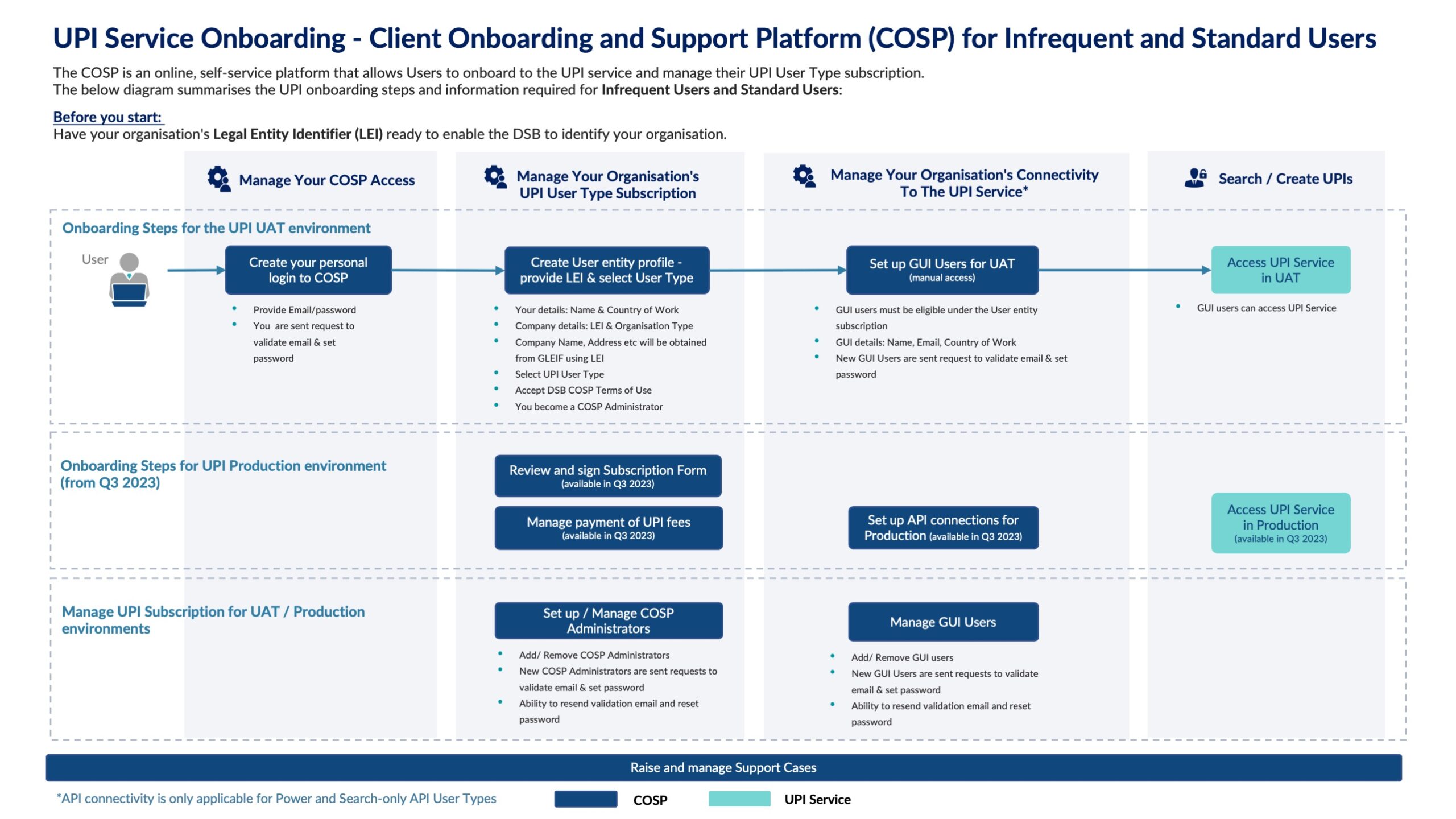

Concerning market preparations for UPI implementation, firms that need access to DSB services will need to consider what kind of DSB connectivity12 they require to cater for UPI integration and data dissemination as part of their reporting workflows.

The DSB is working closely with the ROC on regulatory mandate timelines and expected implementation periods to be offered to market participants and remains geared to aid industry preparation and readiness. The DSB will launch the UPI UAT environment nine months ahead of, and the UPI Service Production environment three months ahead of, the first major derivatives jurisdiction mandate coming into effect.

The UAT launch is anticipated in March 2023, based on the CFTC indicative timelines. The DSB has already finalised the technical specifications13 and legal terms and conditions14 for the UPI Service and stands ready to assist market participants with their technical implementation.

[1] https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=OJ:L:2022:262:TOC

[2] LEI ISO 17442 – https://www.iso.org/standard/78829.html

[3] UPI ISO 4914 – https://www.iso.org/standard/80506.html

[4] UTI ISO 23897 – https://www.iso.org/standard/77308.html

[5] ISIN ISO 6166 – https://www.iso.org/standard/78502.html

[6] https://www.anna-dsb.com/

[7] ISO 10962 – https://www.iso.org/standard/81140.html

[8] ISO 18774 – https://www.iso.org/standard/66153.html

[9] https://www.fsb.org/2019/05/fsb-designates-dsb-as-unique-product-identifier-upi-service-provider/

[10] https://www.leiroc.org/about/index.htm

[11] https://www.cftc.gov/PressRoom/PressReleases/8488-22

[12] https://www.anna-dsb.com/connectivity/

[13] https://www.anna-dsb.com/technical-information/

[14] https://www.anna-dsb.com/upi-legal-terms-and-conditions-consultation/